Health Tech Nerds is one of the most trusted resources in healthcare, helping our members learn, network, build, and grow to maximize our collective impact on the healthcare system.

HTN | Weekly Health Tech Reads | 2/18

This week's newsletter sponsored by: MedallionAs care delivery organizations onboard new providers, many organizations must write off new provider revenue for over 60 days due to lengthy enrollment processes. Given providers average nearly $2,000 in revenue per day, that delay can equate to a loss of $120,000 per provider. With Medallion, this doesn’t have to be reality. In their on-demand webinar, credentialing experts from Medallion will share practical strategies for achieving “day one revenue” and how one organization achieved multiple wins leveraging their provider network management solutions.

If you're interested in sponsoring the newsletter, let us know here.

News

|

Some fresh data from KFF on Medicare Advantage Dual-Eligible Special Needs Plans (D-SNPs) came out last week and includes 10 interesting trends in the space. One chart in particular that caught our attention was the one above, looking at the number of D-SNPs specific plans being offered by major insurers. Notably, it was interesting to see that virtually every major insurer in the D-SNP market has at least doubled the number of plans they offer since 2018.

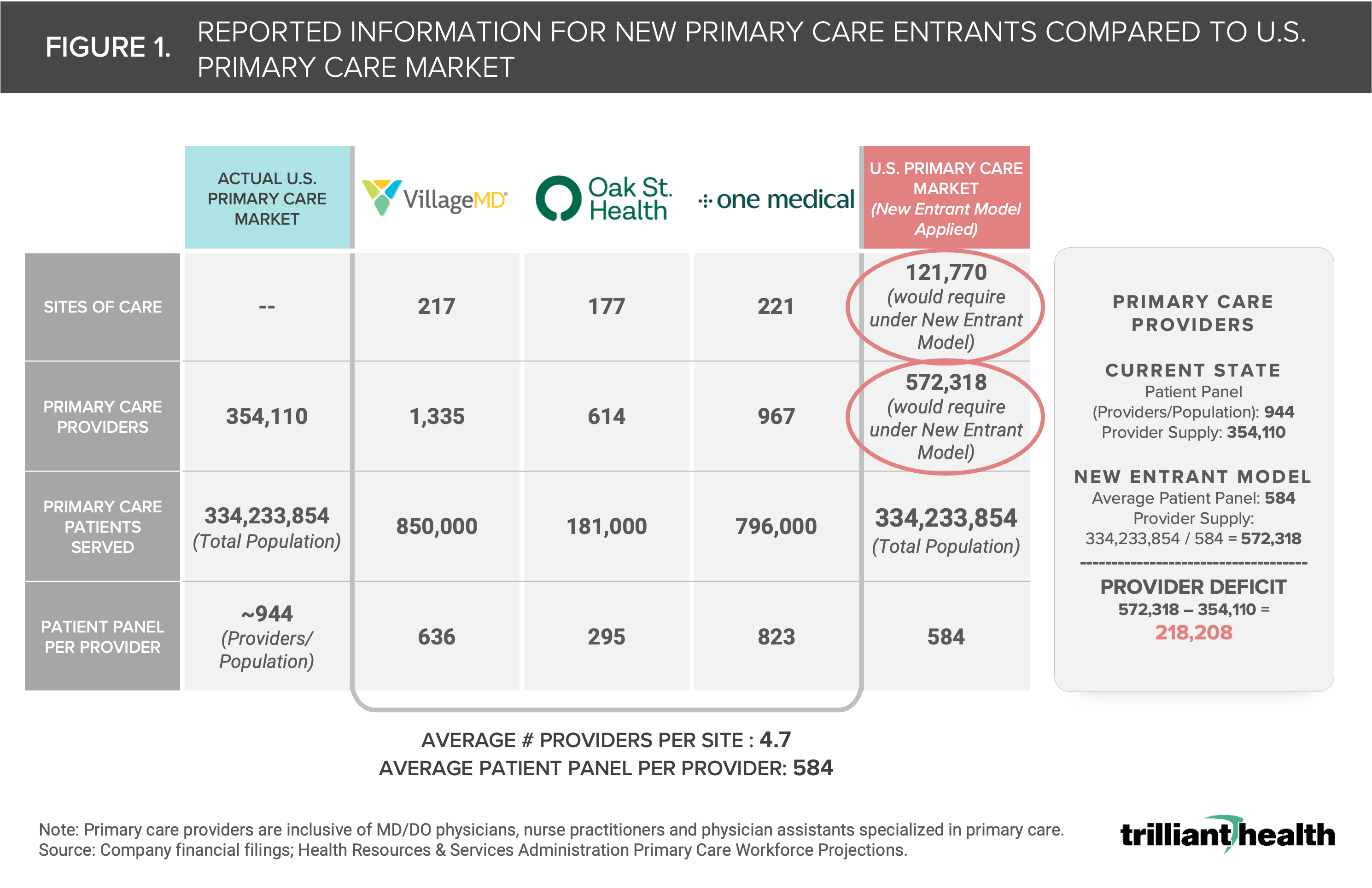

Data on women's and family health benefits offered by employers

This was a comprehensive report on the state of women's and family health benefits from the Maven team, looking at rising costs of healthcare, consolidation benefits trends, employee benefit demands, and more. The report combines results from two surveys conducted from October to November 2023 - with the first collecting data from 1,233 adults in the U.S. and U.K. whose primary area of work is related to the HR and benefits departments and the second aggregated info from 3,077 adults in the same geographies who are employees at companies greater than 500 people. The chart above provides a solid overview of the concentration of current company benefit offerings looks like.

Diving into private equity activity in Medicare Advantage

An interesting deep dive into private equity's involvement in the Medicare Advantage market, looking at deal activity trends, investment drivers & deterrents, company case studies, and more. It's a really great explainer on PE's historical involvement in MA and unpacks how firms actually make money in an ecosystem that is oversaturated by incumbent insurance carriers.

A recent article from KFF looks at the impending squeeze on state Medicaid programs and budgets, signaling a decline in federal Medicaid funding to states' matching funds. The report calls out one particularly concerning number from the recent Congressional Budget Office's Budget and Economic Outlook report - detailing that the CBO projects that states will receive $58 billion less in federal Medicaid outlays in FY 2024 as compared to 2023.

Link / Slack (h/t Avi Aggarwal)

Another healthcare merger fell through this past week with the BCBSLA / Elevance deal being called off. This is the second time in less than a year that the $2.5 billion sale of BCBSLA to Elevance has been scrapped after facing political pushback regarding concerns of the deal's effects on cost and competition in the state.

Link / Slack (h/t Matt Poindexter)

This week was a big week for lawsuits in the news as Advocate Aurora faced a class action for its contracting strategies in Wisconsin. The lawsuit is worth a read if you're looking to understand health system contracting strategies, including things like all-or-nothing clauses and anti-tiering / anti-steering provisions.

Link (summary) / Link (lawsuit)

Freenome, a liquid biopsy company, secured $245 million to advance the development of its single- and multi-cancer detection blood tests.

Link

Anatomy, an AI-enabled financial automation platform, raised $7.6 million. The startup automates healthcare back-office functions by connecting key financial data streams to provide insights into billing and insurance processes.

Link / Slack (h/t Raihan Faroqui)

Dina, an AI-powered care coordination platform, secured $7 million in Series A financing to enhance its platform, expand its national network, and develop new digital care workflows for conditions like chronic congestive heart failure and COPD.

Link

Ilara Health raised $4.2 million in pre-Series A funding. The Kenya-based startup helps private clinics access various medical resources, such as diagnostics devices and pharmaceutical products.

Link

TORTUS, an AI-copilot, secured $4.2 million in fresh capital to build its AI assistant that helps clinicians automate administrative tasks. The company has launched a pilot with Great Ormond Street Hospital for Children NHS Foundation Trust to evaluate the tech in a real-world setting.

Link

.406 Ventures raised $265 million for its fifth fund, with healthcare as one of its three core verticals.

Link

Who Pays for Healthcare AI (Part II) by Morgan Cheatham

The second part of the three part series diving into payment models for healthcare AI. This article covers linear, usage-based, volumetric, bundled services, managed services, and device-maintenance pricing models.

Insights from our Expert Roundtable Series on Oncology by Flare Capital Partners

A great recap of insights and takeaways from Flare Capital's recent Q4'23 roundtable series on oncology. The discussions covered a range of topics, including biopharma & life sciences, plans & providers, startups, technology, and AI.

Chief Medical Officer (CMO), Medicare Advantage Plan at Clover Health, an insuretech company. Link

VP, Care Marketplace at Headspace, a digital mental health provider. Link

SVP of Payer Growth at Sidekick Health, a digital therapeutics startup. Link

Product Manager (US) at Awell, a careops platform. Link

Professional Services Project Manager at Fabric, a healthcare ops enablement platform. Link

Contact us to feature roles in our newsletter.

Welcome to Health Tech Nerds

Health Tech Nerds is one of the most trusted resources in healthcare, helping our members learn, network, build, and grow to maximize our collective impact on the healthcare system.

This week's newsletter sponsored by: Ambience Healthcare Ambience Healthcare’s AI operating system has been deployed at UCSF, Memorial Hermann Health System, John Muir Health, The Oncology Institute, and Eventus WholeHealth. By partnering with Ambience, health systems reduce documentation time by an average of 78%, improve coding integrity, and achieve at least a 5x ROI. Their suite of AI applications includes: AutoScribe: An AI medical scribe tuned by specialty, including the ED AutoCDI: A...

This week's newsletter sponsored by: Sidebar Being a senior leader in healthcare can be lonely. Growing your career in this space requires making a lot of tradeoffs and placing bets on what you believe will have the most impact, then doubling or tripling down on that. As a result, it can be challenging to find time to grow a network of supportive peers. Sidebar is here to help change that. Their vetting process and matching engine pair you with a small group of supportive peers to lean on for...

This week's newsletter sponsored by: Elation Health Elation Health, whose primary care EHR and billing solution supports companies including Crossover Health and Firefly Health, is committed to supporting and advancing the interests of primary care organizations. Recently, Elation was among the coalition of companies advocating for G2211, Medicare’s new billing code that ensures PCPs are adequately compensated for their investment in longitudinal care for patients. Elation’s commitment to...